StatCan: Canada’s per capital output falls 7% down the trend

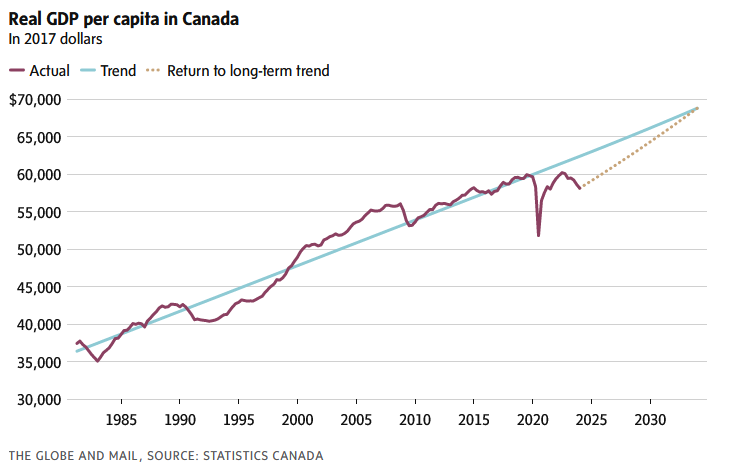

Canada’s economic output on a per capita basis has slipped to 7 per cent below its long-term trend, amounting to a decline of roughly $4,200 a person, according to a report published Wednesday by Statistics Canada.

To return to trend over the next decade, real gross domestic product per capita would need to grow at an average annual rate of 1.7 per cent – similar to the robust expansion in the United States in recent years. The trend for per capita output is based on figures from 1981 through 2023, then extrapolated to 2033.

“Per capita growth of this magnitude is ambitious and a marked departure from recent trends,” wrote Carter McCormack and Weimin Wang, the authors of the report.

Canada’s moribund economic performance on a per person basis has become a flashpoint of discussion over the past couple of years. In a speech last month, Bank of Canada senior deputy governor Carolyn Rogers said the country is facing an “emergency” of weak labour productivity and tepid levels of business investment.

The recent numbers paint a grim picture. Real GDP per capita has fallen to levels seen in 2017. Workers in places with higher per capita output tend to earn higher wages and live longer, making this a popular – if imperfect – measure of a country’s living standards.

The Canadian economy was walloped by COVID-19 in 2020, and more recently, higher interest rates have weighed on growth. At a time of challenging economic conditions, the population is growing at the fastest rates in decades – almost entirely through immigration – which is boosting the denominator in the per capita calculation.

Still, many analysts have said that weaker results aren’t merely a function of the business cycle.

For decades, Canada has struggled with lacklustre capital investment. A Statscan report published in February noted that investment per worker in 2021 was 20 per cent lower than in 2006. During that period, there was a sharp decline in firm entry rates, resulting in weaker competition between companies – and thus, less incentive for them to invest.

Business investment is a critical ingredient for boosting labour productivity, or output per hour worked. In practice, this means workers have more tools at their disposal to help them work more efficiently.

Productivity is the bedrock of per capita growth. Over the four decades leading up to the pandemic, increases in productivity accounted for 93 per cent of the improvement in real GDP per capita, Wednesday’s report said. (Economies can also boost per capita output via higher employment rates and the average employee working longer hours, although these have played a small role in Canada’s long-term gains.)

The trouble for Canada is that labour productivity has faltered of late: While it nudged higher over the final three months of 2023, that followed six consecutive quarters of decline.

“Higher productivity should be everyone’s goal because it’s how we build a better economy for everyone,” Ms. Rogers said in her speech in March. “When a business gives workers better tools and better training, those workers can produce more. That, in turn, means more revenue for the business, which allows it to absorb rising costs, including higher wages, without having to raise prices.”

In its recent budget, the federal government pushed back on some of the pessimism regarding the decline in per capita output. Because newcomers typically earn less than the average Canadian, the government said that the recent influx of people is weighing on average income and productivity. “This should not be misinterpreted to imply that those already in the country are becoming worse off,” the budget read.

Still, the government is now trying to curtail migration to the country, related to concerns over how effectively Canada is absorbing newcomers in key areas, such as housing.

In its latest projections, the Bank of Canada said it expects GDP per capita to decline in the first half of 2024, before picking up in the second half of the year and into early 2025. The central bank said the improvement would be driven by easing financial conditions – the bank is widely expected to lower its policy interest rate around the middle of the year – and rising confidence among consumers and businesses.

Since 1981, real GDP per capita has risen by an average annual rate of 1.1 per cent, the Statscan report said. To return to the long-term trend by 2033, Canada will need to experience a decade of above-average growth.

Strong expansions are not unheard of. From 1991 to 2001, Canada’s real GDP per capita rose at an average annual rate of 2.2 per cent, the Statscan paper said. The implementation of the Canada-U.S. Free Trade Agreement and the adoption of digital technologies helped to spur gains in productivity in the 1990s.

The Statscan authors said it’s an open question of whether emerging technologies will usher in a new era of stronger productivity.

“The ability of Canadian companies to harness the benefits of new competitive technologies related to artificial intelligence, robotics and digitalization will be critical to the link between investment and productivity in the coming years and potentially important contributors to changes in living standards,” they wrote.

This article was first reported by The Globe and Mail